Climate change may still be a debatable science topic for many, but the cost implications of extreme weather events are anything but a passing fad, says the Insurance Bureau of Canada (IBC) vice-president for the Pacific and western regions.

Aaron Sutherland says the occurrence of extreme weather events is increasing along with the damage severity.

“Regardless of what you call it or where it comes from, the impacts are clear, the financial impacts and human toll are clear,” Sutherland said.

Last week, the IBC released its 2023 report on natural disaster insurance payouts across Canada.

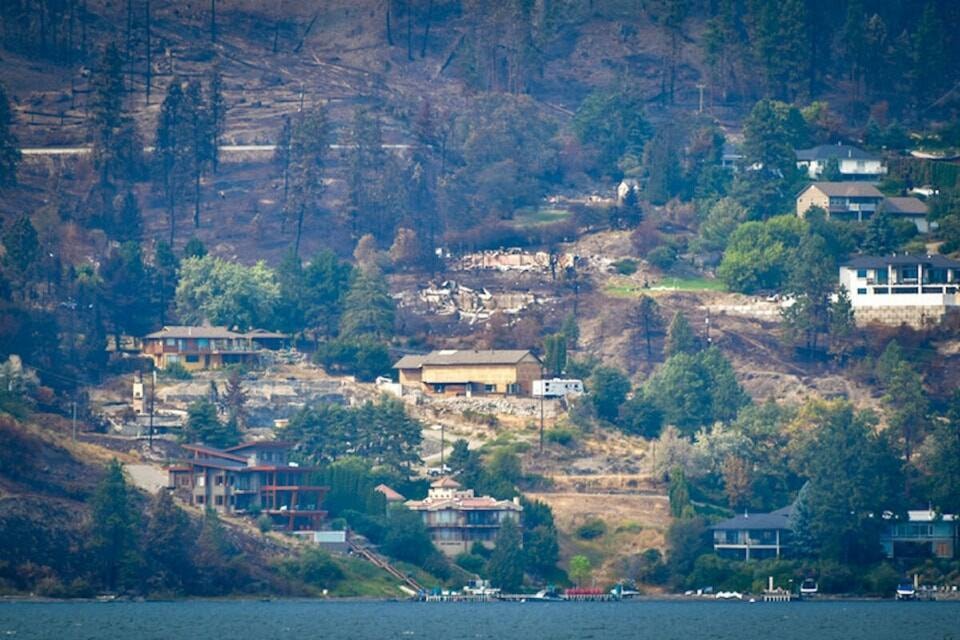

Topping the list were the Okanagan and Shuswap area fires last summer, from Aug. 15 to Sept. 23, which accumulated insurance damage payouts of $720 million.

Second was the severe summer storms in Ontario from July 20 to Aug. 25 at $340 million.

Across Canada, the report estimates that natural catastrophes caused more than $3.1 billion in insured damage, making it the fourth most expensive year on record.

Sutherland says numbers like that catch the attention of the insurance industry, because of the stress it places on insurance premiums to cover potential risk.

“We are concerned about pressure on premiums and we call on all levels of government to begin increasing investments in fire suppression initiatives to reduce that risk,” he said.

“One thing we saw last summer was multiple significant wildfires happening at the same time, such as the Okanagan and Shuswap, which strains the ability of the province to respond. Insurance premiums are a reflection of risk, so the best way to address rising premiums is to address the risk.”

In an interview last summer, Sutherland told Black Press Media while flood insurance is now not offered in some areas because of floodplain exposure, fire insurance still remained the core business of the industry.

The province budgeted $204 million for fire season in 2023, and the cost of fighting those wildfires is expected to exceed $770 million, according to the BC Wildfire Service.

In the U.S., particularly in California and Florida, some insurance brokers have pulled out of certain states because the government-controlled insurance premium limitations make it financially impractical to operate.

In June 2023, American insurance company State Farm announced it would no longer be selling new insurance policies to homeowners in the state of California due to high levels of risk brought on by climate change events such as wildfires and coastal flooding and erosion.

Will we start to see similar moves from the insurance industry in B.C.? Not yet, says Sutherland, but the message should not be ignored.

“We have a different competition model in Canada for insurance and less intervention from the government like you see, for instance, in California,” Sutherland said.

“But it is a cautionary tale of the challenges moving forward as the climate continues to change and we see warmer, dryer, hotter summers year after year and the need for more preventative actions to be taken.”

He said beyond the government doing more to protect infrastructure and private property from extreme weather damage, Sutherland says individual property owners also have a responsibility to weatherproof their homes, starting with following the Firesmart home safety recommendations. “What is required is a multi-faceted solution beyond just investing in bigger dykes or firebreaks.”